Posts

Whether your’re an experienced player or not used to on the web pokies, this article will assist you to come across best game with a high RTP, fun progressive jackpots, and you will enjoyable extra provides. Find respected web sites for Aussie people and methods for selecting the best pokie. Whenever choosing an internet site to find the best on line pokies to try out, makes it subscribed and you can managed. To discover the best alternatives, imagine one of several casinos we listing at the beginning of this site. These types of gambling enterprises are highly recommended and gives a variety of genuine currency pokies and expert customer care. Play at the all of our online pokies a real income web sites to own a spin to victory cash honors on the many games.

They were the brand new gambling enterprises one to constantly obtained more than mediocre in almost any key town, not merely one. Over your subscription within just a minute or two from the typing some basic info just like your identity, many years, current email address, and you can popular money. Particular casinos also can ask for your own address and you may contact number to own confirmation.

Why Microgaming Casinos in australia Are nevertheless My Best Alternatives

Volatility is also important to imagine because will help you to plan learning to make your money past. Pokies don’t have of a lot options, but the partners there exists https://australianfreepokies.com/free-bonus-slots/ features an effect to the the fresh to experience experience. National Gambling establishment brings a variety of fee tips, as well as playing cards, e-Wallets, and you may cryptocurrencies including Bitcoin and you can Litecoin. Places is small and easy, when you are withdrawals are also prompt, even though profiles must over KYC verification prior to its earliest bucks-away.

Speak about Old Egypt inside Yggdrasil slot to see pyramids, pharaohs, and you will powerful gods in style. Expanding reels, multipliers, and you may respins are among the invisible secrets where you are able to winnings to 5,800x the new share. It step three-reel, 5-payline position from Betsoft has Hold & Win respins, in which collecting Zeus’ coins can be open jackpot honors. Appreciate 100 percent free revolves, wilds, a great 96.18% RTP and huge jackpot of 1,000x your share. The option is quicker but i have lots of internet sites we recommend to possess Screen mobile pages. One more thing to mention is how the brand new artwork plus affiliate experience is actually affected by monitor size.

Spin Palace

That it point will present more popular business to help you Australian viewers. The companies listed below are famous because of their exceptional a real income on line pokies and now have gotten multiple certifications and you will honors for their successes. We just consider subscribed casinos on the internet for real money that have rigid defense standards. They’re the use of 128-portion Safer Sockets Coating (SSL) encryption app. SSL protects all of the correspondence between the browser and the local casino’s net server.

🎯 Editor’s Take: Smarter Pokies Play for Large Perks

Like that you’ll have a reassurance as you gain benefit from the thrill of to try out a favourite pokies the real deal money. For individuals who’lso are trying to gamble pokies, black-jack or any other gambling games, then you’ll definitely need to discover a seller you to allows participants from your latest place. Simultaneously, we should find a reliable gambling enterprise site that gives a great high group of game and you will ample bonuses to make to experience truth be told there since the enjoyable and you will effective to. Leading online gambling internet sites play with Haphazard Number Creator (RNG) application to make sure reasonable performance on every twist. Separate audits by the firms such as eCOGRA ensure this type of standards are often maintained. Here at VegasSlotsOnline, i simply approve on the internet pokies real money gambling enterprises you to definitely follow reasonable play.

Greatest Spot to Win in the On line Pokies

To help you get started finding the optimum on the internet pokies, here is the best pokie internet sites open to Australians. Here you can find brief ratings in our top web sites in order to rapidly find out what for each and every has to offer. Only see which is right for you and you may initiate to experience right away anyway. Very casinos on the internet enable it to be the newest professionals to help you bet on their favorite video game without betting requirements. Some of the subjects there’s is just how and you will where to find the profitable pokies, ideas on how to play, recommendations, status, and much more. We are purchased bringing simply exact advice as well as the safest, safest on the internet pokies sites.

- The fresh judge land is principally shaped by the Entertaining Playing Act 2001, and this regulates gambling on line things all over the country.

- If you like reputable managed and you may registered websites, you will delight in a premium experience without shelter concerns.

- Gaming in the Oz try a famous hobby, and there’s absolutely nothing like to experience pokies on line for real currency.

- Improvements pubs, ranks ladders, plus-video game success render incentives a game title-such as framework one to features lessons entertaining and you will customized.

- Studying viewpoints is one of effective way to look at information about advised on line Australian position games.

Following the basic phase, 32 casinos were taken off thought, so we began tracking information about the remaining 104 authorized gambling enterprises. All the twist, detachment, extra identity, and you will assistance communication are signed, timed, and you can rated. From that point, i set up a comparison system in order to get per user around the trick categories, along with earnings, cellular feel, online game assortment, and you can support effect times.

Last Suggestions to Get you off and running With On line Pokies

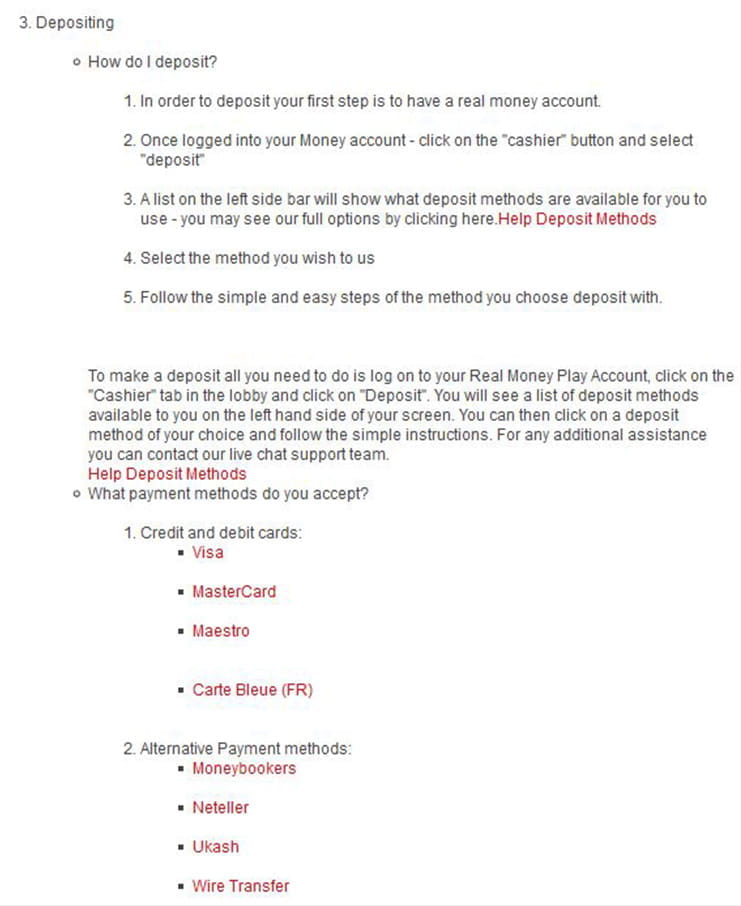

Choose the method that you need to put cash in your casino membership to make the first deposit. This can be plus the time to claim any greeting bonuses the new casino now offers so you can start to play a popular online game that have a real income. For those who’re trying to find an informed on the web pokies within the The fresh Zealand, the fresh Pokies Online people provides everything you need and more. We make an effort to become an entire financing for Kiwi internet casino followers whom like to play real on the internet pokies.